Subscribe!

Don’t Leave Money on the Table: Trump Accounts are Live — Politics and Confusion Should Not Keep Families Away

by RINewsToday News Team

Trump Accounts are now live, and for families with children, this is one of those financial steps that should not get lost in the noise of politics, paperwork, summer distractions — or the name of the program.

As the stock market opened Monday, President Trump marked the launch of the accounts from the White House. The program began on July 4, the 250th birthday of the United States, and is now available for families to open and manage through the official Trump Accounts system.

The name may get all the attention. But this is not about a bumper sticker, a yard sign, or a political argument at the dinner table. It is about a child’s savings and investment account, in the child’s name, designed to give American children an early start in building long-term financial security.

For some families, that start could include $1,000 from the federal government. For others, it could include a $250 private philanthropic contribution. For all eligible children under 18, it creates a new long-term investment option that parents, grandparents, family members, employers and others may be able to help fund over time.

And yet, a new BabyCenter survey suggests a surprising number of families may skip the opportunity — some knowingly, some unknowingly.

According to BabyCenter, more than 1 in 4 eligible mothers surveyed — 27% — said they plan to forgo Trump Accounts and the $1,000 government contribution for newborns. Another 20% said they are unaware of what the accounts are or what they do. BabyCenter characterizes that as nearly half of eligible families potentially missing out, either by intention or by lack of awareness.

Politics appears to be part of it. BabyCenter says 17% of mothers who plan to open the account say they are doing so only for the money, even though they do not support the current administration. Gen Z parents were also more likely to reject the accounts for political reasons, according to the survey, with 16% saying they would not sign up because they do not support the administration, compared with 8% of Millennial parents.

There is also an income and awareness gap. BabyCenter says families earning $125,000 or more are far more likely to use the accounts than families earning under $75,000. It also found that nearly 1 in 3 parents earning under $75,000 were unaware of what a Trump Account is.

See the report: https://www.babycenter.com/family/money/trump-accounts_41003824

The families most likely to benefit from free seed money, small contributions and long-term growth may also be among the families least likely to know the program exists.

So here is the practical breakdown.

Not just for newborns

The $1,000 federal Treasury contribution is for eligible U.S. citizen children born from January 1, 2025, through December 31, 2028, who have a valid Social Security number.

But Trump Accounts themselves are not only for newborns.

The IRS describes Trump Accounts as a new type of individual retirement account for children. An account may be opened for a child who has not turned 18 before the end of the calendar year in which the election is made and who has a valid Social Security number.

That means parents of older children should not stop reading just because their child was born before 2025.

There are really three categories to understand:

First, any child under 18 with a valid Social Security number may be eligible to have a Trump Account opened.

Second, children born from 2025 through 2028 may qualify for the one-time $1,000 federal Treasury contribution.

Third, some older children may qualify for a separate private contribution. Michael and Susan Dell have pledged $6.25 billion to provide $250 each to the first 25 million qualifying children age 10 and under who live in ZIP codes with median incomes below $150,000. That $250 is separate from the federal $1,000 newborn contribution.

That point matters. The BabyCenter survey focuses heavily on the $1,000 newborn contribution, but families with children outside the 2025–2028 birth window may still have a reason to open an account.

How to start

Families can begin through TrumpAccounts.gov, the official Trump Accounts app, or the IRS online account system. The IRS says the process should take about 5 to 10 minutes.

The person opening the account will need an ID.me account, the child’s Social Security number, and the child’s date of birth and address. The IRS form used to elect a child is Form 4547.

Families should be careful to use only official sites and official app links. Do not click random social media links, text-message links, email offers, or lookalike websites asking for a child’s Social Security number or family banking information.

What the app does

Treasury announced that the full Trump Accounts app is now live nationwide. The app allows parents and children to securely access accounts, see funds in real time, and contribute directly from a phone or tablet.

It includes dashboards showing balances, contributions and investment performance, along with tools to link bank accounts and set recurring contributions.

Treasury says the app also includes 15 interactive financial education modules for parents and children, covering saving, investing, compound growth, diversification and how markets work.

That educational piece may turn out to be one of the strongest parts of the program. Children can grow up seeing the account, tracking the investment and learning that saving is not just something “other people” do.

Small money can become real money

Once the account is activated, the important part begins: putting money in and leaving it alone long enough to grow.

Parents, family and friends may contribute to a child’s Trump Account, up to a combined total of $5,000 per year. Employers may also contribute, with special rules for employer contributions. Certain government and nonprofit contributions may also be allowed.

That means this does not have to be only a parent’s project.

A grandparent can make a birthday contribution. An aunt or uncle can add something at Christmas. A family friend can help. A business owner can look at whether this might become a family-friendly employee benefit.

One of the most painless ways a parent can contribute is to set up a small recurring contribution — even $25 a month, or $25 a pay period — to go directly into the account.

It is reminiscent of how schools used to sell savings bonds. Children brought in small amounts over time, and when there was enough for a bond, they received something tangible to take home. The lesson was not just the value of the bond. The lesson was the habit.

The same idea applies here.

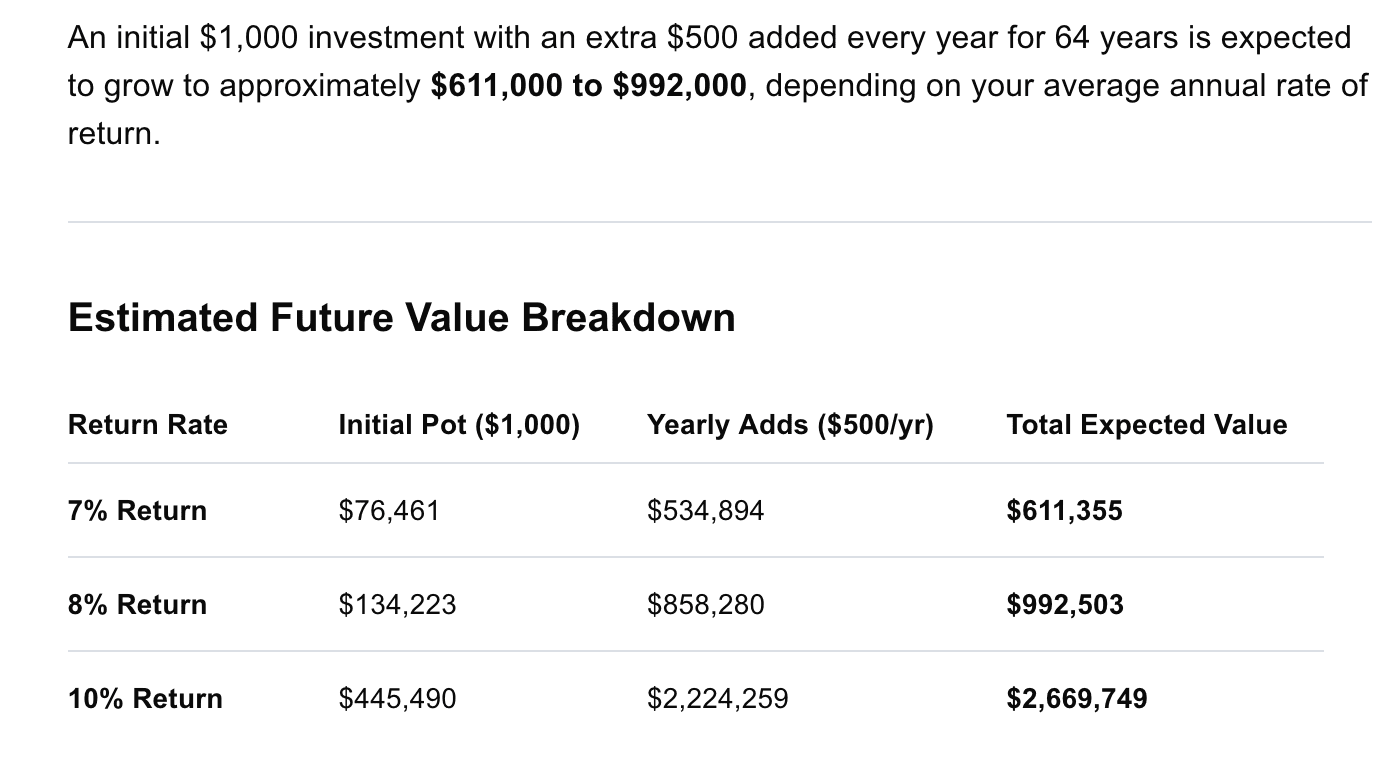

A family does not have to start with $50 a month. Even $25 a month can become meaningful. Small deposits plus many years can become real money.

The official Trump Accounts example shows how a newborn’s account that starts with the $1,000 Treasury contribution and then receives $50 per month for 18 years, assuming a 7% average annual return, could grow to about $25,048 by age 18. That is an illustration, not a guarantee, but it shows the power of time and consistency.

A family that can only do $25 a month should not dismiss the idea. A monthly transfer that happens quietly in the background can do more than a big intention that never gets started.

Birthdays, holidays and grandparents

Families can also think differently about birthdays and holidays.

Instead of another toy, another outfit, or another gadget that will be forgotten, grandparents and relatives can put part of the gift into the child’s account. The child can still get a present to open, but the account gets a present for the future.

A birthday card that says, “We put $25 into your account,” may not excite a toddler. But it may matter a great deal when that toddler is 18, 25 or 40.

And for grandparents who want to do something practical, this is a way to give without waiting until a will, an estate, or a crisis. It lets them participate in a child’s future while the child is growing.

Employers should pay attention

Employers should pay attention, too.

Treasury says more than 50 companies have already committed to offer Trump Account contributions for children of their employees. Employer contributions may be available even for children who do not qualify for the $1,000 Treasury contribution, making this more than a newborn-only benefit.

For small businesses, this could become a new kind of family-friendly benefit. With employers competing for reliable workers, benefits that help employees’ children may stand out.

A contribution does not have to be huge to be meaningful. Even modest employer contributions, repeated over years, can help a child’s account grow.

How the money is invested

At launch, Treasury says all Trump Account contributions will initially be invested in the State Street SPDR Portfolio S&P 500 ETF, known by the ticker SPYM. It is a low-cost exchange-traded fund designed to track the S&P 500, giving children broad exposure to the U.S. stock market.

Treasury has also announced four additional low-cost index fund options expected to become available in the coming months: iShares Core S&P 500 ETF, Vanguard Total Stock Market ETF, State Street SPDR Portfolio S&P 1500 Composite Stock Market ETF, and iShares Core Total U.S. Stock Market ETF.

Until the new selection feature is available, contributions will remain in the default State Street fund.

In plain English: this is not a stock-picking account, and families are not being asked to choose individual companies. The money is being directed into broad, low-cost U.S. market index funds — the kind of long-term investment many retirement savers already use.

That also means families should understand the risk. This is an investment account. Markets go up and down. Returns are not guaranteed. The value of the account can rise and fall over time.

But for children, time is the key advantage.

What happens at 18

Before the child reaches 18, withdrawals are generally restricted.

After the child reaches 18, the account generally transitions to traditional IRA rules. Funds may be used without the additional 10% early distribution tax for certain eligible expenses, such as higher education expenses or a first-time home purchase of up to $10,000 lifetime, though ordinary income tax may still apply. Other withdrawals may trigger taxes and penalties.

It may help with education. It may help with a first home. It may become retirement money. It may simply teach a child, early, that investing is something regular people can do.

Parents should also remember that a Trump Account does not replace every other savings option. A 529 plan may still make more sense for families focused specifically on college or other qualified education expenses. A regular savings account may still be needed for short-term needs.

A Trump Account is different. It is designed to get children started with long-term investing, even before they have earned income of their own.

Politics, paperwork and the child’s future

The name of the account is political. That is unavoidable.

But the account itself belongs to the child.

That is the practical question parents have to answer. Should a parent’s politics keep a child from receiving money that could help with education, a first home, a business idea, or retirement decades from now?

Families can dislike the name. They can dislike the politics. They can still take the money for the child.

That may be especially important for lower-income families, where BabyCenter’s survey suggests awareness is lower and participation may lag behind higher-income households. A family with fewer resources may not be able to contribute $5,000 a year. That does not mean the family should walk away from $1,000, $250, or the possibility of small contributions over time.

Do not wait because $25 feels too small. Do not wait because you cannot contribute the maximum. Do not wait because politics give you pause.

Open the account if your child is eligible. Claim the $1,000 if your child qualifies. Check whether your older child may qualify for the $250 Dell contribution. Ask whether an employer will contribute. Invite grandparents and family to help. Then use the account not only to track money, but to teach the child what saving, investing and patience can do over time.

The account belongs to the child.

The opportunity belongs to the child.

And the growth, years from now, will belong to the child when they are making grown-up decisions about education, home buying, work, family and retirement.

As with all investment decisions, families should consult tax or financial advisers for personal advice; investment returns are not guaranteed.