Subscribe!

RIPEC Report: RI Cities, Towns Continue to Shift Burden to Increasing Property Taxes

|

|

|

___

Given these findings, RIPEC makes the following recommendations to state and local policymakers:

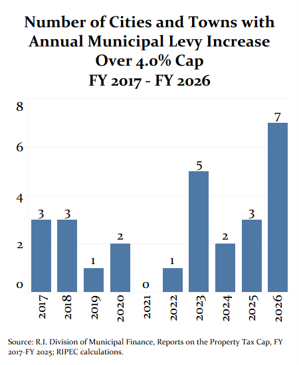

The state should maintain the 4.0 percent levy cap. The cap is one of the few components of Rhode Island’s property tax system that places relatively uniform limits on cities and towns, and shields taxpayers from sharp year-over-year increases in their property tax bills. State policymakers should maintain this important protection.

The state should adopt a constitutional amendment that sets guardrails limiting effective tax rate differentials across property classes. Rhode Island has a state classification plan that sets limits to tax differentials, but most cities and towns have an exemption, or an individual statute, allowing deviation from state requirements. Ultimately, state statutes have proven ineffective at reducing, or even maintaining, current tax rate differentials, exacerbating unfairness among taxpayers and worsening housing affordability and economic opportunity in Rhode Island.

State policymakers should consider implementing an annual property revaluation schedule. The more frequently property is assessed, the more accurate are assessments relative to market value. Rhode Island is currently experiencing large swings in valuation that render three-year-old assessments highly inaccurate. This creates another layer of unfairness among taxpayers and may result in policy decisions being influenced by price shock. This unfairness among taxpayers will soon be compounded by the new state tax on higher-value non-owner-occupied residential property, as assessed values will diverge from market values by varying degrees across communities based on revaluation cycles.

Local policymakers should consider adopting or expanding targeted methods of property tax relief. When broad relief is provided to all homeowners without regard for ability to pay, property tax systems become distortive and unfair relative to other taxpayers. However, given that property is a non-liquid asset, property tax increases based solely on property value can be particularly burdensome to some taxpayers. Targeted tax relief can serve as a better tool to assist overly burdened taxpayers. Most municipalities already make use of means-tested tax relief programs—such as freezes, deferrals, and credits—and expanded use of these tools would better equip local governments to target tax relief.